Exemptions Information

Exemptions Information

Generally, initial application for property tax exemption must be made between January 1 and March 1 of the year for which the exemption is sought. Initial application can be made online or in person at the property appraiser's office.

General Exemptions

Homestead Exemption provides qualified applicants with a reduction in their home's taxable value up to $25,000. Applicants may file for Homestead Exemption between November 1st and March 1st of the year in which the benefit will be applied. Once approved, Homestead Exemption is automatically renewed each year as long as ownership and residence conditions remain the same for the property.

REQUIREMENTS:

Article VII, Section 6 of the Florida Constitution provides that all property owners who, as of January 1, have legal or equitable title to real estate and maintain it as their permanent residence, are entitled to a $25,000 Homestead Exemption, or a percentage thereof if the ownership interest is less than 100%. Only one Homestead Exemption is allowed to any individual or family unit.

To receive Homestead Exemption, applicants must qualify on or before January 1st and submit an application with the Property Appraiser on or before March 1st of the year in which the benefit will be applied.

IMPORTANT: Homestead Exemption does not automatically transfer to a new residence. Florida law requires property owners to file a new application if they move or if they change the manner in which title is held on their existing homestead.

Required Documents for all Applicants:

- Florida driver's license, or, if you do not drive, a Florida identification card

- Florida vehicle registration for vehicles owned or leased by you

- Hardee County voter registration card, if you are registered to vote

- If you are not a U.S. citizen, a permanent resident alien card ('green card') is needed

- If property is in trust, a copy of the trust agreement or a copy of a recorded memorandum of trust If the applicant owns property in any other state or country, a letter may be required from the appropriate agency verifying that the applicant does not receive benefits based on permanent residency in that jurisdiction

- If the homestead is a manufactured home, registration(s) or title(s) for the manufactured home

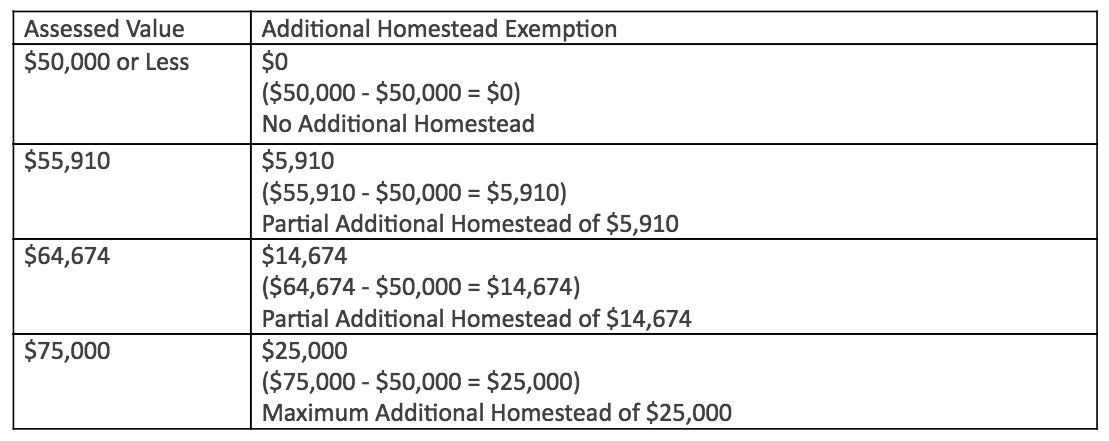

The Additional Homestead Exemption provides qualified applicants with an additional reduction in their home's taxable value up to $25,000 each year.

REQUIREMENTS:

The Additional Homestead Exemption is automatically applied to any property that receives the original $25,000 Homestead Exemption. To receive the full $25,000 benefit of the Additional Homestead Exemption, the property's assessed value must be at least $75,000. If the assessed value is less than $75,000, the Additional Homestead Exemption will be less than $25,000. Homestead Exemption is required for this exemption.

Required Documents for all Applicants:

Learn more about § 196.031(1)(b)

Learn more about § 196.031(1)(b)

- Florida driver's license, or, if you do not drive, a Florida identification card

- Florida vehicle registration for all vehicles owned or leased by you, or registered to your business

- Hardee County voter registration card, if you are registered to vote Social Security card or other official document that includes the social security number. (Social Security documentation is required for the spouse of each applicant even if applicant’s spouse has no ownership interest in the homestead property)

- If you are not a U.S. citizen, a permanent resident alien card ('green card') is needed

- If property is in trust, a copy of the trust agreement or a copy of a recorded memorandum of trust If the applicant owns property in any other state or country, a letter may be required from the appropriate agency verifying that the applicant does not receive benefits based on permanent residency in that jurisdiction

- If the homestead is a manufactured home, registration(s) or title(s) for the manufactured home

Learn more about § 196.031(1)(b)

Learn more about § 196.031(1)(b)

The Widow/Widower Exemption provides qualified applicants with up to a $5000 reduction in taxable value on one property they own.

REQUIREMENTS:

- Must be a widow or widower prior to January 1st of the year in which the exemption will be applied

- Cannot be remarried

- Must be a permanent resident of Florida

- Must provide a copy of the spouse's death certificate

The Blind Persons Exemption provides qualified applicants with up to a $5000 reduction in taxable value on one property they own.

REQUIREMENTS:

An applicant for the $5000 Blind Persons Exemption must be a permanent resident of Florida and provide an Optometrist's Certification of Disability, a certificate from the Division of Blind Services, the United States Department of Veterans Affairs, or the Social Security Administration, certifying the applicant to be blind.

Homestead Exemption is not required for this exemption.

Homestead Exemption is not required for this exemption.

Learn more about § 196.202

The $5000 Disability Exemption provides qualified applicants with up to a $5000 reduction in taxable value on one property they own.

REQUIREMENTS:

An applicant for the $5000 Disability Exemption must be a permanent resident of Florida and provide a Physician's Certificate from one Florida licensed doctor, or documentation from the Social Security Administration.

Homestead Exemption is not required for this exemption.

Learn more about § 196.202

The Total & Permanent Disability Exemption for Civilians provides qualified applicants with up to 100% exemption from all ad-valorem property taxes.

REQUIREMENTS:

- Any real estate used and owned as a homestead by any quadriplegic is exempt from taxation.

- Must be a paraplegic, hemiplegic, or other total and permanent disability requiring the applicant to be confined to a wheel chair for mobility, or who is legally blind

- Must have an adjusted household income not exceeding an amount determined annually by the Department of Revenue based on the Consumer Price Index and provided to the Property Appraiser mid-January each year

- Must provide a Physician's Certificate from two, non-affiliated, licensed Florida doctors

- Must provide an annual affirmation of income to retain this benefit (Quadriplegics do not need to meet the income requirements.) Income limitations

The Limited-Income Seniors Exemption provides an additional exemption for residents age 65-years and older who do not exceed state-mandated maximum income.

Article VII of the Constitution of the State of Florida gives authority to the Board of County Commissioners and municipal governments to determine the benefit amount, not to exceed $50,000.

Hardee County and all municipalities each provide a $25,000 exemption offering between $222 - $436 depending on the tax rates and tax district.

REQUIREMENTS:

- Must be 65-years old or older on or by January 1 of the current roll year

- Must have an adjusted household income not exceeding an amount determined annually by the Department of Revenue based on the Consumer Price Index and provided to the Property Appraiser mid-January each year

- Must file an initial application with the Property Appraiser’s office

- Must provide a copy of the prior year's Federal income tax returns - if filed, and include any wage and earning statements (W-2, 1099) Income limitations

Non-Profit Exemptions

Non-Profit Exemption provides qualified organizations with up to 100% exemption from all ad-valorem property taxes.

REQUIREMENTS

The organization must file an original application for exemption with the Property Appraiser between January 1st and March 1st.

The organizations must fit certain definitions and meet criteria of Chapter 196 of the Florida Statutes, such as:

- Must have legal title on January 1st

- Must use the property for an exempt purpose on January 1st

- The organization using property for religious, literary, scientific, or charitable purposes must be non-profit § 196.195 (4)Property Appraisers look at financial information provided and look at the reasonableness of salaries, charges for services rendered in relation to value of services, and other items to determine whether property is used for profit making purposes § 196.195 (2)

- A copy of the organization's federal tax return (if filed), and an annual income & expense statement or annual budget

- A copy of a valid 501(c)(3) Internal Revenue Service determination (churches without 501(c)(3) exempt)

- A copy of a valid Consumer Certificate of Exemption from the Florida Department of Revenue (a/k/a sales tax exemption certificate)

- A copy of the Articles of Incorporation or Articles of Organization, and by-laws

The Non-Profit Exemption for churches provides qualified applicants with up to 100% exemption from all ad-valorem property taxes.

REQUIREMENTS

Requirements for Churches are the same as requirements for all non-profit organizations, with the addition of the following:

- A copy of determination letter for religious organizations that have obtained an IRS 501(c)(3) designation

- A copy of the Church Charter, if one exists

- Copies of Church bulletins if they assist in establishing how the property was used on January 1st of the year in which they are applying

The Non-Profit Exemption for Charter Schools provides qualified applicants with up to 100% exemption from all ad-valorem property taxes.

REQUIREMENTS

Requirements for Charter Schools are the same as requirements for all non-profit organizations, with the addition of the following:

- Must file application form DR-504CS if the charter school rents space

Must file application form DR-504CS if the charter school rents space

REQUIREMENTS

Requirements for Homes for the Aged are the same as requirements for all non-profit organizations, with the addition of the following as governed by Florida Statute § 196.1975

- Must file application form DR-504HA instead of filing the DR-504 application

- Must provide affidavits form DR_504S, which includes each tenant’s income, age and disability, if any, and affirms the tenant is a permanent resident of Florida, and considers the unit their permanent resident. Tenants cannot retain a homestead exemption on any other property

- Must provide a spreadsheet or letter that summarizes the contents of the tenant affidavits.

The Non-Profit Exemption for Affordable Housing provides qualified applicants with up to 100% exemption from all ad-valorem property taxes.

REQUIREMENTS

Requirements for Affordable Housing are the same as requirements for all non-profit organizations, with the addition of the following as governed by Florida Statute § 196.1978

- Tenant Spreadsheet that includes the unit number, tenant name, original lease or move-in date, household income verification date, total number of household occupants, total annual gross income for entire household, monthly rent, monthly rent contributed by tenant, utility allowance, whether they receive section 8 subsidy, and number of bedrooms.

- Tenant Spreadsheet that includes the unit number, tenant name, original lease or move-in date, household income verification date, total number of household occupants, total annual gross income for entire household, monthly rent, monthly rent contributed by tenant, utility allowance, whether they receive section 8 subsidy, and number of bedrooms.

Conservation Exemptions

Florida law provides two methods of property tax relief for conservation land. In both cases, the land must meet the requirements of a conservation easement as defined in § 704.06.

Easements may be granted to government agencies or charitable organizations whose purpose is to protect natural, scenic or open space; assuring availability of agricultural, forest, recreational or open space use; or protecting natural resources. It is usually perpetual, but could be for a term of no less than 10 years.

It prohibits any or all of the following activities and uses:

- Building

- Dumping

- Clearing

- Excavation

- Surface Use

Applies to conservation easements with a term of no less than 10 years. Instrument must be recorded with the Clerk of Court. A copy must be submitted with application. Once an original application is granted, the owner is not required to file a renewal application if there is no change in use.

Learn more about § 193.501

Applies to conservation easements into perpetuity. Land under easement that is used for commercial purposes is exempt to the extent of 50% of the assessed value. Land under 40 contiguous acres must be determined by ARC (Acquisition and Restoration Council), a State agency. Once an original application is granted, the owner is not required to file a renewal application if there is no change in use.

Learn more about § 196.26

The property owner must apply for assessment or exemption on the appropriate form.

Land Used For Conservation Assessment Application Form DR-482C

Real Property Dedicated In Perpetuity For Conservation Exemption Application Form DR-418C

The Application deadline is March 1.